Where to go next

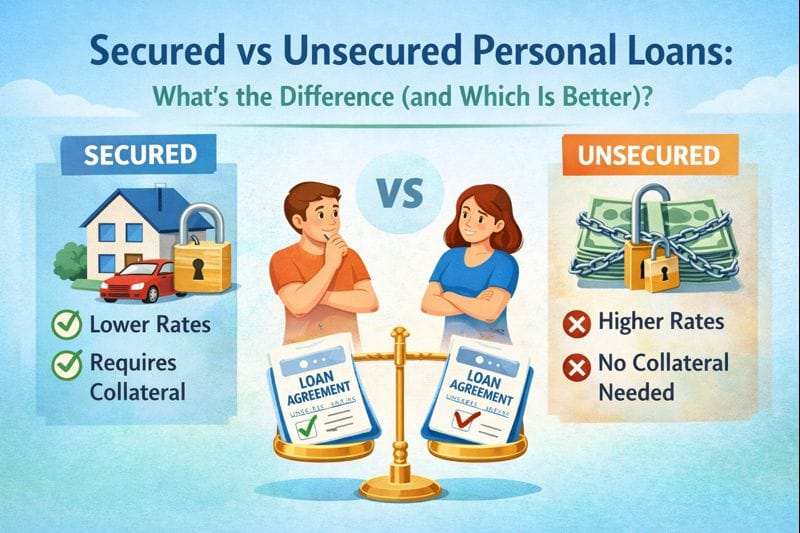

A personal loan can be unsecured (no collateral) or secured (backed by something you own). Secured loans can sometimes be easier to qualify for or cheaper—because the lender has a fallback. But that fallback is your asset. If you miss payments, you can lose it.

This guide explains secured vs unsecured personal loans, what collateral really means, what lenders care about for approval, and how to choose without making one bad month turn into a disaster.

Quick answer / Key takeaways

- Unsecured loans don’t require collateral; approval depends mostly on credit, income, and DTI.

- Secured loans require collateral; they may improve approval odds and sometimes lower APR.

- The real risk of a secured loan is losing the asset if you default.

- A secured loan is rarely smart if it puts essential assets at risk (car you need for work, savings you can’t replace).

- Always compare total cost (APR + fees + term), not just “approved.”

How to compare loan offers

What is a secured personal loan?

A secured personal loan is backed by collateral—an asset that the lender can claim if you default.

Secured loan collateral (common examples)

This answers your tail: “secured loan collateral.”

Collateral can include things like:

- cash savings in an account (sometimes called a “share-secured” loan at a credit union)

- a vehicle title (higher risk)

- other pledged assets depending on the lender

The key point: collateral makes the loan safer for the lender, not for you.

What is an unsecured personal loan?

An unsecured personal loan is not backed by collateral. The lender relies on:

- your credit history

- income verification

- DTI

- overall credit file stability

Requirements + docs: Personal loan requirements documents

DTI basics: dti for personal loans

Unsecured loan approval factors (what lenders look at)

This answers your tail: “unsecured loan approval factors.”

Most lenders focus on:

- credit score and recent history

- income and job stability (or predictable income sources)

- DTI (how much debt you already carry relative to income)

- recent inquiries/new accounts

If any of these are weak, the lender may:

- raise APR,

- reduce loan amount,

- require a co-signer, or

- deny the application.

Co-signer guide: cosigner joint loans

Secured vs unsecured: which is better?

This answers your tail: “which is better.”

Unsecured is usually better if:

- you qualify for a reasonable APR without collateral, and

- you want to keep your assets out of the deal.

Secured can be better if:

- your credit is weak and unsecured offers are extremely expensive, and

- the collateral is something you can afford to risk (or it’s cash-secured), and

- the APR drop is meaningful enough to justify the added risk.

Secured is usually a bad idea if:

- the collateral is essential (car needed for work), or

- you’re using collateral to cover a payment you can’t truly afford.

Table: Secured vs unsecured personal loans (side-by-side)

| Category | Secured personal loan | Unsecured personal loan |

|---|---|---|

| Collateral required | Yes | No |

| Approval odds | Often easier if collateral is strong | Depends heavily on credit/income/DTI |

| APR (typical) | Sometimes lower | Often higher if credit is weaker |

| Loan amount | May be tied to collateral value | Tied to credit profile + income |

| Biggest risk | Lose the collateral if you default | Credit damage + collections if you default |

| Best for | Borrowers who need approval help and can risk the collateral | Borrowers who qualify on credit/income alone |

| Worst fit | Anyone risking essential assets | Anyone with very weak credit and no payment buffer |

How to choose (step-by-step)

Step 1: Check if you qualify for an unsecured loan first

Start with prequalification to see likely terms without committing to a hard pull.

Prequalify soft pull

Step 2: Compare unsecured offers by total cost

Use APR + fees + term + total repaid.

How to compare loan offers

Personal loan fees

Step 3: If unsecured pricing is extreme, evaluate secured

Ask:

- What collateral is required?

- What happens if I miss one payment?

- How fast can the lender take the asset?

- Is the APR difference big enough to justify the risk?

Step 4: Never secure a loan with something you can’t afford to lose

If losing the collateral would wreck your life (job, housing stability), don’t do it.

Step 5: Lock in a payment you can survive

A secured loan doesn’t fix affordability. If the payment is tight, it’s still a bad loan.

DTI and payment safety: dti for personal loans

Costs to watch (fees and penalties)

Secured or unsecured, fees can make a “good rate” expensive:

- origination fees

- late fees

- prepayment penalties

If you plan to pay early, confirm there’s no penalty:

- Early payoff & refinancing — early payoff refinance

Common mistakes

- Using a secured loan to “buy approval” when the payment still isn’t affordable.

- Pledging an essential asset (car) and turning one missed payment into a crisis.

- Ignoring fees that reduce net funding or increase cost.

- Choosing the longest term just to lower payment (then overpaying total interest).

Examples / scenarios (If X → do Y)

Scenario 1: “Unsecured offers are insanely expensive.”

Prequalify and compare. If unsecured APR is extreme, a cash-secured loan (where the collateral is savings) can sometimes reduce cost with less chaos than risking a car. But don’t do it if it empties your emergency cushion.

Scenario 2: “I can qualify unsecured but the secured rate is slightly lower.”

If the difference is small, don’t add collateral risk for minor savings. Keep assets out of it.

Scenario 3: “I’m considering a title-secured loan.”

Treat it as high risk. If losing the vehicle would break your income, don’t do it. Look at safer alternatives or borrow less.

FAQ

What is the difference between a secured and unsecured personal loan?

A secured loan requires collateral that the lender can take if you default. An unsecured loan does not require collateral and relies on credit/income/DTI for approval.

Are secured loans easier to get?

Often yes, because collateral reduces lender risk. But “easier approval” doesn’t mean it’s safer for you.

Do secured loans always have lower interest rates?

Not always. Sometimes the rate is only slightly lower—always compare total cost and risk.

Can I lose my collateral on a secured personal loan?

Yes. If you default, the lender may seize the collateral depending on the loan terms and local rules.

Which is better: secured or unsecured?

Unsecured is usually better if you qualify for reasonable terms. Secured may help if unsecured options are extreme and you can afford the collateral risk.