Where to go next

Prequalifying is how you shop personal loan offers without firing blind hard inquiries everywhere. If you do it right, you can see likely APR/payment ranges first, then apply only where the deal actually makes sense.

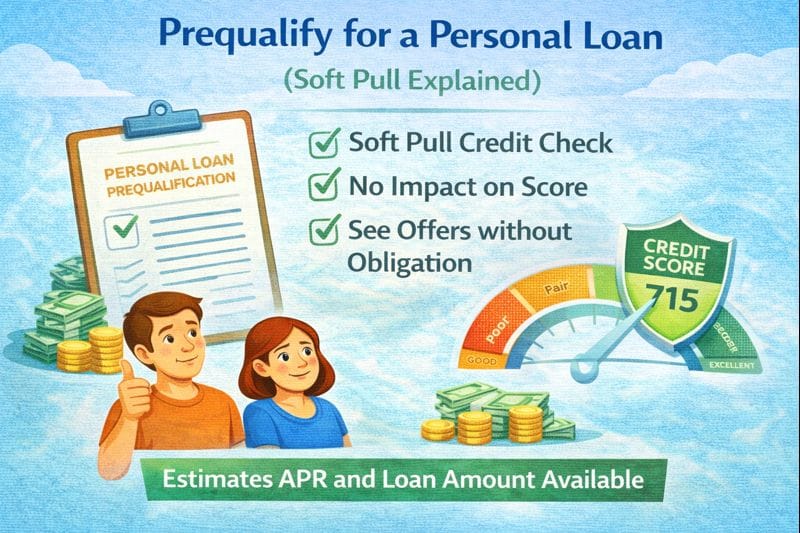

This guide explains what it means to prequalify for a personal loan, how soft pull prequalification works, whether prequalifying hurts your credit, and how pre-approval differs from prequalify.

Quick answer / Key takeaways

- Prequalification often uses a soft pull to estimate offers and typically does not hurt your score.

- A full application usually triggers a hard inquiry (that’s the one that can move your score).

- Prequalify first, then apply only to the best offers to limit hard pulls.

- Pre-approval and prequalification are not always the same—terms vary by lender.

- Still compare offers by total cost, not just APR or payment: how to compare loan offers.

What does it mean to prequalify for a personal loan?

Prequalification is an initial screening that estimates what you might qualify for based on:

- basic identity and income info you provide, and

- a credit check that is often a soft pull.

It’s designed to reduce guesswork. It’s not always a guarantee.

If you’re new to how personal loans work:

how personal loans work.

Prequalification soft pull (how it works)

This answers your tail: “prequalification soft pull.”

Soft pull = “look but don’t commit”

A soft pull is a credit check that generally doesn’t affect your score the way a hard inquiry can.

What you typically get from prequal

- estimated APR range

- estimated monthly payment range

- possible loan amounts and terms

- sometimes the likelihood of approval

What can change after prequal

Final terms can change after:

- full identity verification

- income verification

- final underwriting

- the lender runs a hard inquiry and confirms your full file

Requirements and docs that can affect final approval:

personal loan requirements documents.

Does prequalifying hurt your credit?

This answers your tail: “does prequalifying hurt credit.”

Usually, prequalifying does not hurt your credit if it’s a soft pull. But you should still read the lender’s wording before you submit.

Rule you can follow:

If it says “soft credit check” or “no impact to your score,” that’s the safer prequal path.

If it says “this will not affect your credit score” but later asks for a full application, the hard inquiry comes later.

Hard inquiry breakdown: hard inquiry impact.

Pre-approval vs prequalify (what’s the difference?)

This answers your tail: “pre-approval vs prequalify.”

These terms are used inconsistently. Here’s the practical difference.

Prequalification (often lighter)

- usually a soft pull

- gives estimated offers

- less documentation up front

- not always a firm commitment

Pre-approval (often stronger, but not always)

- may involve more verification

- may be closer to a final offer

- may still require a hard inquiry or final underwriting step

Practical takeaway: treat both as “not final” until you see the final offer and loan agreement.

How to prequalify the smart way (step-by-step)

Step 1: Get your numbers straight

Know:

- how much you need,

- your target payment,

- your purpose (consolidation, big expense, etc.).

If you’re consolidating, start here:

debt consolidation loans.

Step 2: Prequalify with multiple lenders (but keep it organized)

Keep a simple list of offers with:

- APR range

- fees (especially origination fees)

- term length options

- estimated payment

- any special conditions

Fees guide: personal loan fees.

Origination fee deep dive: origination fee explained.

Step 3: Shortlist the best offers

Cut it down to the top 1–3 based on total cost and payment comfort.

Step 4: Apply only where it makes sense

This is how you limit hard inquiries.

hard inquiry impact.

Step 5: Verify final terms before accepting

Final checklist:

- APR and interest rate

- origination fee and net funding amount

- late fee rules

- prepayment penalty rules

- total amount repaid

Offer comparison checklist: how to compare loan offers.

Table: Prequalify vs apply (what changes)

| Stage | Credit check type | What you get | Risk |

|---|---|---|---|

| Prequalify | Often soft pull | Estimated offers | Not final; terms can change |

| Full application | Often hard inquiry | Final decision + terms | Can affect score; denial possible |

| Funding/closing | Verification + contract | Money disbursed | Fees/terms locked in |

Common mistakes

- Prequalifying and treating the offer as guaranteed.

- Applying everywhere instead of shortlisting (stacking hard inquiries).

- Comparing only monthly payment and ignoring fees/total cost.

How to compare loan offers. - Ignoring DTI and getting denied even with decent credit.

Dti for personal loans.

Examples / scenarios

Scenario 1: “I want the best rate without hurting my score.”

Prequalify with several lenders, shortlist, then apply only to the best one or two.

Hard inquiry impact.

Scenario 2: “I got prequalified but denied later.”

Usually verification didn’t match: income, DTI, or identity. Prep documents and re-apply strategically.

Personal loan requirements documents.

Scenario 3: “I’m consolidating and need a specific payoff amount.”

Prequal offers aren’t enough—confirm origination fee and net funding in final terms.

Origination fee explained.

FAQ

What does it mean to prequalify for a personal loan?

It’s an initial screening that estimates likely loan offers, often using a soft credit pull.

Does prequalifying hurt your credit?

Usually no if it’s a soft pull. A hard inquiry typically happens at the full application stage.

Is pre-approval the same as prequalification?

Not always. Pre-approval may involve more verification and may be closer to final terms, but it still might not be final.

Should I prequalify with multiple lenders?

Yes, if it’s soft pull and you stay organized—then apply only to the best offers.

What should I compare after prequalifying?

APR, fees (especially origination), term length, monthly payment, and total cost.

How to compare loan offers.